Featured

March 6, 2017

See how paying more than the minimum balance can help your pay down your debt faster and reduce your interest.

March 6, 2017

t’s a number we hear about a lot. Your credit score. Everyone is talking about it (including those guys that sing about it on TV), but […]

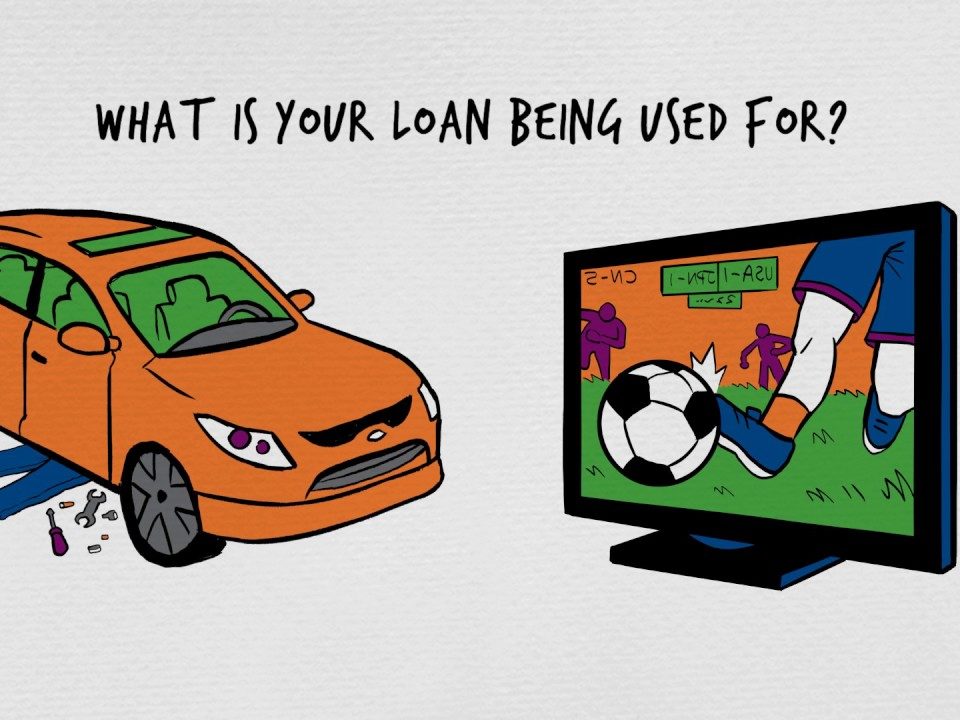

Understand Loans

March 6, 2017

Aquí se explica porqué no debe pagarle a un negocio que promote bajar los pagos mensuales del préstamo para su carro y ayudarlo a parar el […]

March 6, 2017

Este video demuestra lo que sucede cuando alguien consigue un préstamo de día de pago y no puede pagar la deuda en la fecha de vencimiento.

March 6, 2017

When cash is tight, some people turn to payday and similar loans to make ends meet. For some people payday loans become debt traps and our […]

March 6, 2017

Este video demuestra lo que sucede si usted cambio el título de su vehículo por un préstamo.

March 6, 2017

March 6, 2017

Learn about borrowing money for the things you need, interest and fees, and payment schedules.

March 6, 2017

This video shows what happens when someone makes just the minimum payment on a credit card balance.

Improve Credit

March 6, 2017

Credit is on the minds of many. According to the National Foundation for Credit Counseling’s (NFCC) 2013 Financial Literacy Survey, 19% of Americans are worried about […]

March 6, 2017

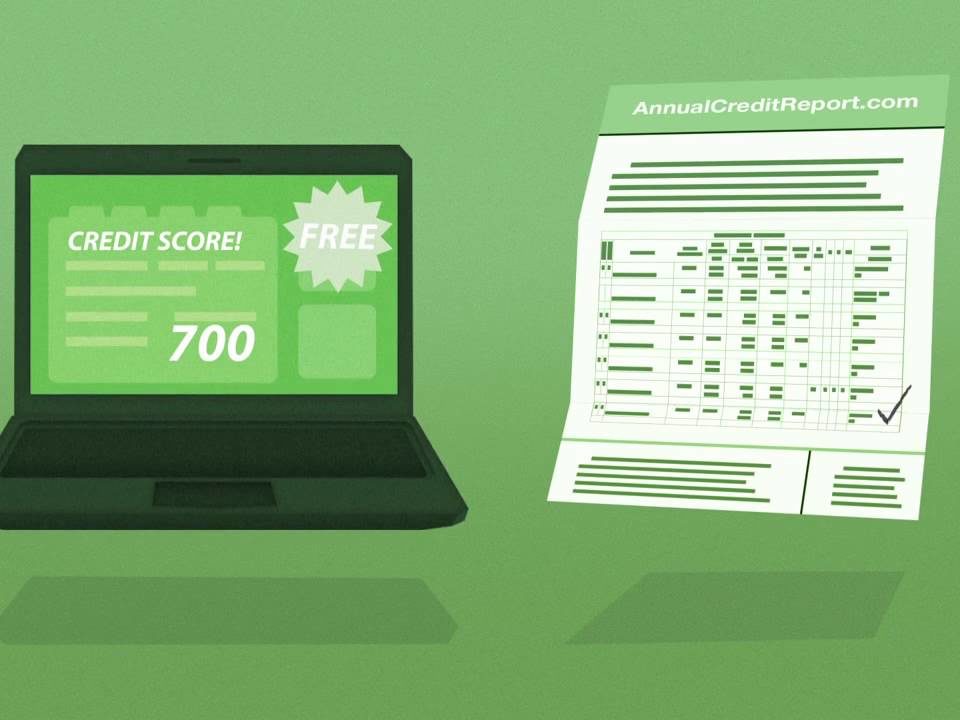

Your credit report affects your ability to get a loan or job, and could help you avoid identity theft. You can get a truly free credit […]

March 6, 2017

An FTC video about why you should check your credit report and what to do about any errors you find.

March 6, 2017

Este video demuestra cómo alquilar un apartamento aunque no tenga un buen historial de crédito.

March 6, 2017

Su informe de crédito afecta su habilidad de obtener un préstamo o empleo, y puede ayudarle evitar el robo de identidad. Usted puede obtener un informe […]

Use Banking Products

March 6, 2017

This video shows how someone compares the costs when choosing a place open savings and checking accounts.

March 6, 2017

Este video muestra lo que ocurre cuando alguien obtiene una tarjeta de prepago sin comprobar los cargos en primer lugar.

March 6, 2017

Este video muestra cómo alguien compara los costos al momento de elegir un lugar de ahorro y cuentas corrientes abiertas.

March 6, 2017

This video shows what happens when someone gets a prepaid card without checking out the fees first.

Reduce Student Debt

March 6, 2017

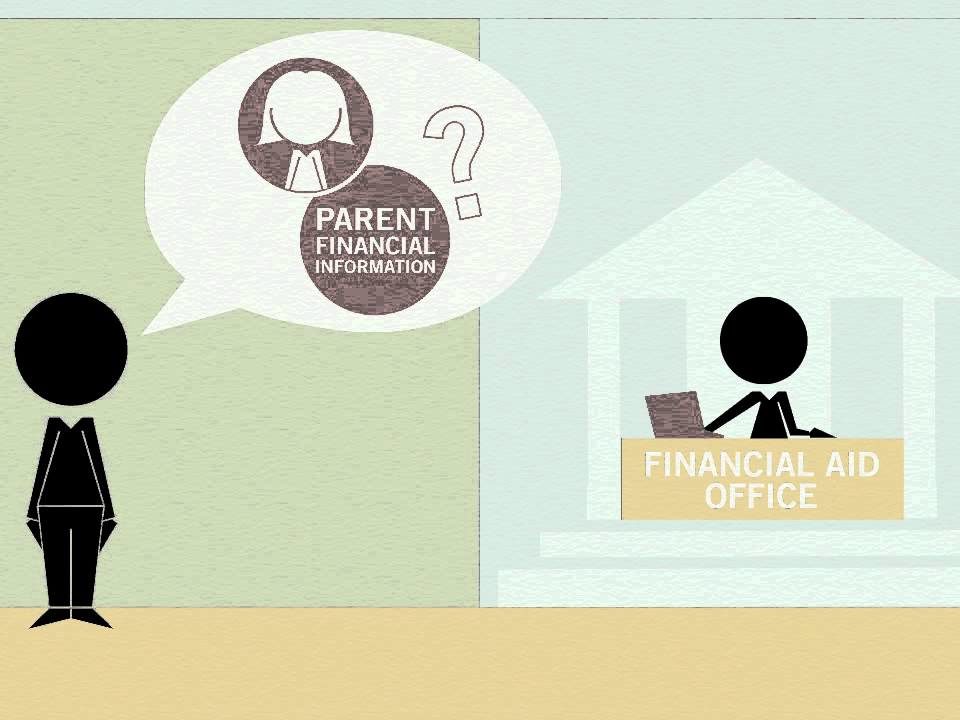

Are you ready to complete the Free Application for Federal Student Aid, but are unsure whether you’ll need to provide parental information on the form? Check […]

March 6, 2017

Check out this video to learn how the Free Application for Federal Student Aid (FAFSA) gives you access to grants, loans and work-study jobs that can […]

March 6, 2017

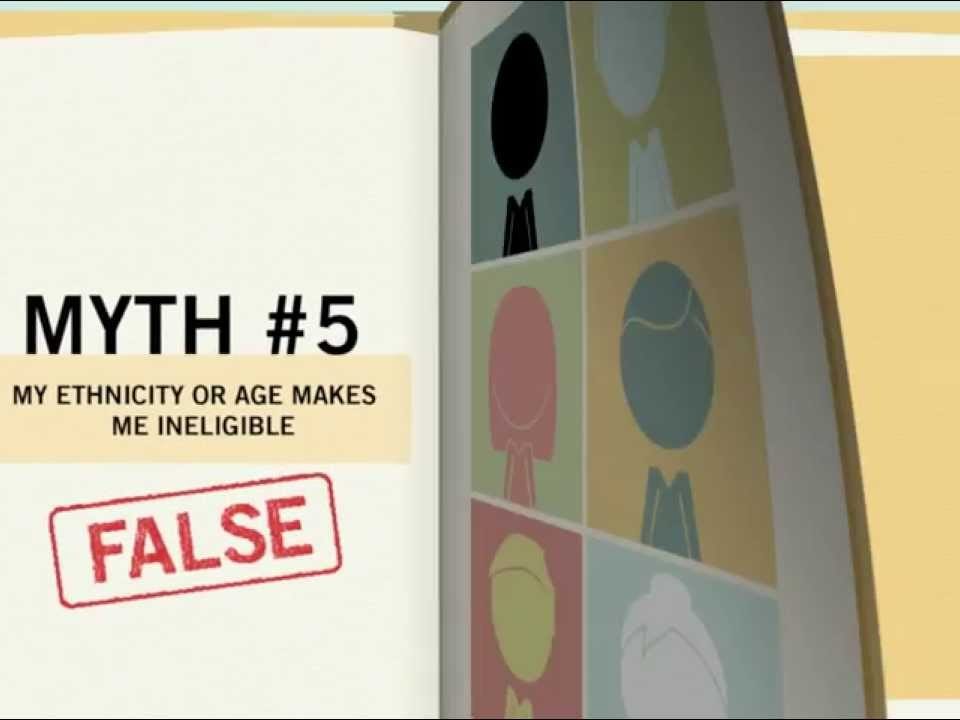

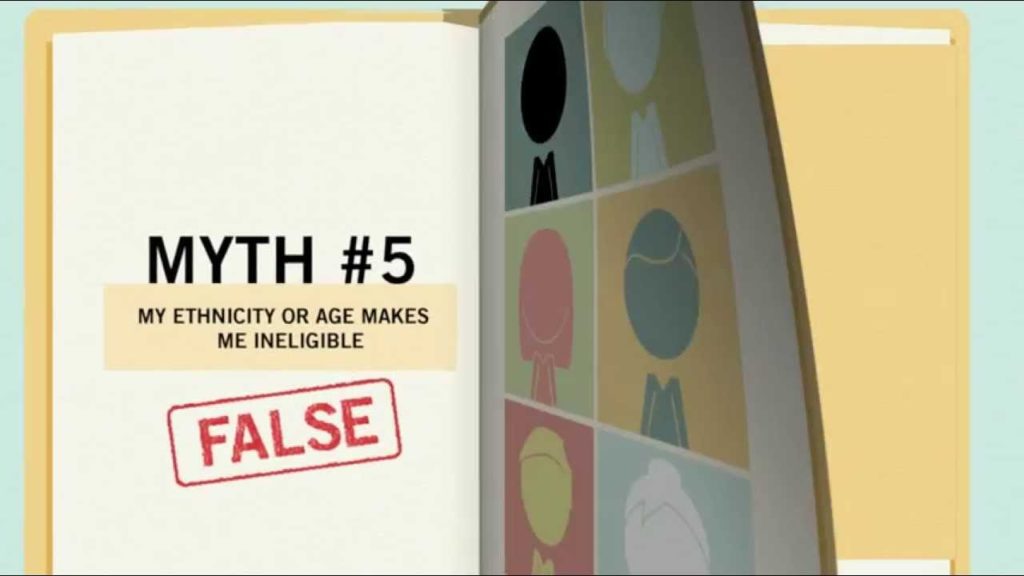

Ready for college, but not sure how to pay for it? Don’t let these myths about federal student aid keep you from applying for and getting […]

March 6, 2017

The first step to applying for federal student aid is completing the Free Application for Federal Student Aid (or the FAFSA®). Before you fill out your […]

March 6, 2017

The Free Application for Federal Student Aid (FAFSA) allows students to apply for more than $150 billion in grants, loans, and work-study funds. Check out this […]

March 6, 2017

If you’re having trouble making payments on your federal student loans, we have several options available to help you manage your debt. Check out this video […]

March 6, 2017

Are you ready to attend college or career school, but need financial aid to help fund your education? Check out this video to learn how the […]

March 6, 2017

Are you unsure about the loan repayment process or wondering when you need to begin making loan payments? Check out this video to learn about what […]

March 6, 2017

Are you thinking about taking out a federal student loan to help pay for college or career school? Check out this video to learn about your […]

March 6, 2017

If you need help paying for college or career school, the office of Federal Student Aid can assist you with getting the money you need. Check […]

Avoid Scams

March 6, 2017

March 6, 2017

Imposters promise romance to users of online dating sites to trick them into sending money. Learn more about online romance imposter scams at https://www.ftc.gov/imposters

March 6, 2017

Callers impersonate legitimate technical support companies to fool computer users into handing over their personal information or sending money. Learn more about tech support imposter scams […]

March 6, 2017

Routine steps we can all take to protect our personal information and reduce our risk of identity theft. Learn more about protecting your identity and recovering […]

March 6, 2017

How to spot scammers who pretend to be IRS officials to get you to send them money. Learn more about IRS imposter scams at https://www.ftc.gov/imposters

March 6, 2017

The immediate steps a victim should take to limit the damage caused by an identity thief.

March 6, 2017

Pasos rutinarios que todos podemos seguir para proteger nuestra información personal y reducir el riesgo del robo de identidad.

March 6, 2017

Este video muestra lo que sucede cuando alguien aprende de la manera difícil por qué deben preocuparse por su identidad.

March 6, 2017

Car ads might promise low payments, no interest, or zero down. But is there a catch? Here’s what you need to know.

Recovering from ID Theft

Saving and Investing

March 6, 2017

Getting the facts about a used car before you buy can help avoid trouble down the road. Here’s what you need to know.

March 6, 2017

Compound interest is often called one of the most powerful concepts in finance. Find out what it is and how it can work for you.

March 6, 2017

Este vídeo muestra cómo mantener un presupuesto le ayuda a alguien a pagar todas sus cuentas.

March 6, 2017

Mutual funds are the starting point for many individual investors because they offer a balanced portfolio in a single investment. Find out how mutual funds work […]

March 6, 2017

We’re all saving for something and Philadelphia Saves can help! The free program allows you to set savings goals, and have access to online tools to […]

March 6, 2017

The time value of money is a fundamental concept in finance – and it influences every financial decision you make, whether you know it or not. […]

March 6, 2017

Income investors love them and growth investors rarely expect them, but just what are dividends? Learn the story behind these payouts and why they are (or […]

File Taxes

March 6, 2017

Doing your taxes doesn’t have to be taxing. Do your federal taxes with IRS Free File: Brand–name software plus secure e-filing—all for free! Available 24/7 on […]

March 6, 2017

As April 15th approaches, many people are filing their taxes and looking forward to pocketing their refund checks. This year, the average tax refund is $3,053. […]

March 6, 2017

Finding out you owe when you expected a refund is a nasty shock. Find out how to cope with the bad news.

March 6, 2017

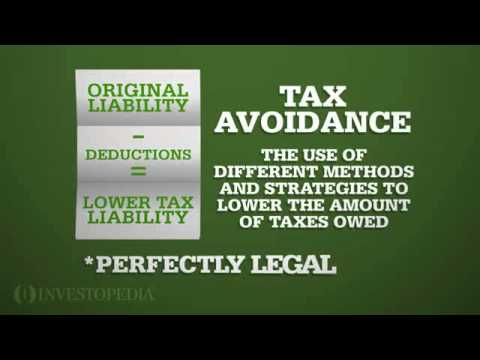

Evading taxes is illegal, but avoiding paying unnecessary tax is one of the keys to building wealth.

March 6, 2017

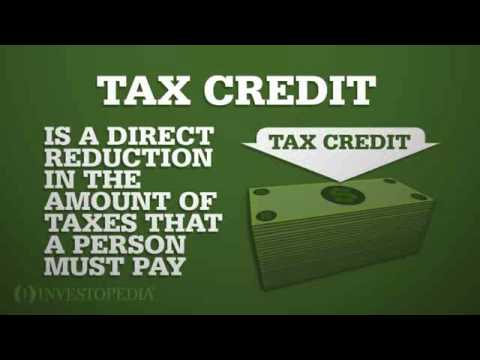

You might not know this (yet), but there are some key differences between tax “deductions” and tax “credits” — we outline these differences here.

March 6, 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Refund anticipation checks are often offered by tax preparers as a way to get your tax refund faster than normal—especially if you don’t have a bank […]